Cross-Border Payments & Product Compliance for Ecommerce: What UK & EU Brands Need to Know

Essential guidance on VAT compliance, cross-border payments compliance, and responsible person ecommerce requirements to ensure seamless transactions in the UK and EU.

Expanding into UK and EU markets represents a significant growth opportunity for ecommerce brands, but success hinges on more than just product-market fit.

Behind every cross-border transaction lies a complex web of cross-border payments compliance requirements, tax obligations, and regulatory frameworks that can make or break your market entry strategy. Getting both VAT compliance cross-border ecommerce and product compliance right, simultaneously, is the defining challenge for brands scaling internationally.

For finance directors, ecommerce operations managers, and compliance officers, understanding the intersection of payments and compliance is critical. A misstep in either area can result in delayed shipments, frozen funds, regulatory penalties, or even market exclusion. This guide provides the essential framework you need to navigate these challenges confidently.

The Dual Challenge: Cross-Border Payments Compliance and Product Compliance

When entering UK and EU markets, brands face a dual challenge that requires coordinated strategy:

- Payment Complexity: Managing multi-currency transactions, navigating varied payment preferences, ensuring VAT compliance cross-border ecommerce obligations, and optimising for local payment methods while maintaining healthy cash flow.

- Regulatory Compliance: Meeting product compliance UK EU standards, proper labelling requirements, appointing responsible persons, and registering products in local databases before goods can legally enter the market.

These two dimensions are intrinsically linked. You cannot process payments efficiently if your products are held at customs due to compliance issues. Equally, achieving compliance is futile if your payment infrastructure cannot support the transaction volumes and tax requirements of your target markets.

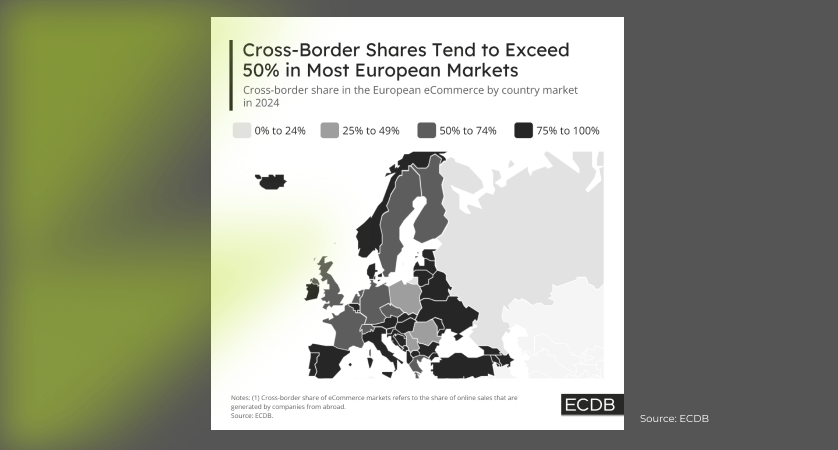

Understanding Cross-Border Payment Dynamics in the UK and EU

Multi-Currency Considerations

Operating across UK and EU markets means managing transactions in GBP and EUR, with implications for:

- Exchange rate risk: Currency fluctuations can significantly impact margins, particularly for businesses operating on thin profit margins

- Settlement timing: Different payment methods have varying settlement periods, affecting cash flow management

- Customer expectations: Local consumers expect to see prices and pay in their local currency

Strategic approach: Implement dynamic currency conversion with transparent exchange rates, and consider hedging strategies for larger transaction volumes. Build buffer margins to account for currency volatility.

VAT Compliance: Cross-Border Ecommerce Requirements

One of the most complex aspects of cross-border payments compliance is navigating the distinct VAT frameworks of the UK and EU. Getting VAT compliance cross-border ecommerce right is non-negotiable and errors carry significant penalties.

EU VAT Landscape:

- Standard VAT rates range from 17% to 27% across member states

- One Stop Shop (OSS) scheme simplifies multi-country VAT reporting for distance sales up to €10,000 per country

- Beyond thresholds, you may need individual country registrations

- Import One Stop Shop (IOSS) for goods under €150 imported from outside the EU

UK VAT Requirements:

- Standard rate of 20% on most goods

- VAT registration required when taxable turnover exceeds £90,000

- Post-Brexit import VAT and customs duty considerations

- Postponed VAT accounting available for imports

Critical consideration: VAT collection at point of sale is mandatory for most distance sales. Your payment system must be configured to calculate, collect, and report VAT correctly across jurisdictions. Errors here can lead to significant penalties and reputational damage.

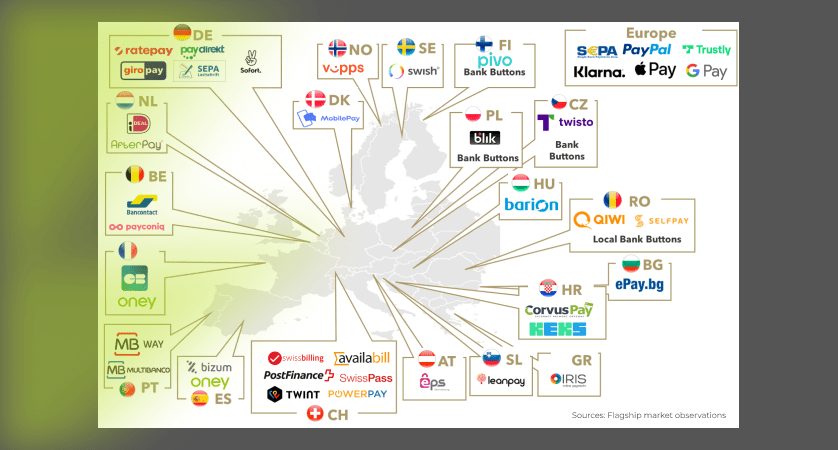

Payment Method Localisation

Payment preferences vary significantly across markets:

- UK: Credit/debit cards dominate, with growing adoption of digital wallets like Apple Pay and Google Pay

- Netherlands: iDEAL is essential, used in over 60% of online transactions

- Germany: Strong preference for invoice-based payments and direct bank transfers

- Nordics: Mobile payment solutions like Swish (Sweden) and MobilePay (Denmark)

Strategic approach: Partner with payment providers that offer comprehensive local payment method support. Each additional payment method can increase conversion rates by 5–15% in its target market.

Product Compliance UK EU: The Gateway to Market Access

While payment infrastructure is essential, it’s meaningless if your products cannot legally enter and be sold in your target markets. Product compliance UK EU is not optional, it is the foundation upon which all market entry is built.

Responsible Person Ecommerce Requirements

One of the most critical but often overlooked aspects of responsible person ecommerce compliance is the mandatory appointment of a Responsible Person (RP) for non-UK and non-EU brands.

- What is a Responsible Person? A legal entity based in the UK or EU that takes responsibility for ensuring products comply with relevant regulations. For non-UK/EU manufacturers, this is a mandatory requirement for most product categories.

Why responsible person ecommerce obligations matter for payments:

- Without proper RP designation, products may be seized at customs, creating payment disputes and refund obligations

- Marketplace platforms (Amazon, eBay, etc.) increasingly require proof of RP before allowing listings

- Payment holds can occur if compliance documentation is questioned during routine checks

Category-Specific Product Compliance UK EU Requirements

Different product categories face distinct regulatory frameworks under product compliance UK EU rules:

- Cosmetics and Personal Care: Product Information Files (PIF) mandatory; registration in EU CPNP and UK SCPN databases; comprehensive ingredient compliance reviews; specific labelling requirements

- Dietary Supplements and Food: Novel food authorisations where applicable; health claim substantiation; allergen declarations; country-specific product registrations

- Consumer Electronics: CE marking for EU, UKCA marking for UK; electromagnetic compatibility testing; safety documentation and technical files

- Chemicals and Textiles: REACH and CLP compliance; restricted substance testing; safety data sheets (SDS); sustainability and environmental standards

- Toys and Children’s Products: EN71 safety standards; age-appropriate labelling; choking hazard assessments

The Compliance Timeline Challenge

Many brands underestimate the time required for product compliance UK EU approval:

- Documentation gathering: 2–4 weeks

- Regulatory review and testing: 4–8 weeks

- Database registrations: 2–6 weeks

- Labelling updates and reprinting: 2–4 weeks

Total timeline: 10–22 weeks from start to market-ready status. This directly impacts your cross-border payments compliance and cash flow planning, inventory purchased but unable to be sold due to compliance delays represents locked capital and storage costs.

The Financial Impact of Non-Compliance

Understanding the financial consequences of compliance failures is essential for finance directors and operations managers:

Direct Costs

- Product seizures: Complete loss of inventory value plus disposal fees

- Customs penalties: Can reach thousands of pounds per violation

- Reshipment and storage: Costs for returned goods and warehousing

- Marketplace suspension fees: Lost sales during account holds

- Legal representation: Costs to resolve regulatory disputes

Indirect Costs

- Customer refunds and compensation: Cancelled orders due to delivery failures

- Brand reputation damage: Reviews and ratings impacted by delivery problems

- Lost sales velocity: Algorithm penalties on marketplaces

- Payment processor scrutiny: Increased reserves or holds due to high dispute rates

- Market re-entry costs: Additional compliance work and testing after violations

A practical example: A cosmetics brand entering the EU market without proper CPNP registration could see their first shipment of 5,000 units (valued at €150,000) seized at customs. Total financial impact would exceed €200,000 when including disposal fees, rush compliance costs, second production run, and six months of lost market opportunity.

Best Practices for Finance Directors and Operations Managers

1. Treat Compliance as a Payment Enabler

Don’t view product compliance UK EU as a separate silo from your payment operations. Compliance documentation enables cross-border payments compliance by ensuring goods flow freely across borders. Budget for both simultaneously and track them as interdependent metrics.

2. Build Compliance Costs into Product Pricing

Factor compliance costs into your unit economics from day one:

- Responsible Person fees (typically £1,000–5,000 annually)

- Testing and assessment costs (£500–5,000 per product line)

- Database registration fees (varies by category)

- Ongoing monitoring and updates

3. Implement Clear Internal Handoffs

Define clear ownership and communication protocols between:

- Finance (payment processing, VAT compliance cross-border ecommerce, reconciliation)

- Operations (inventory management, compliance documentation)

- Legal/Compliance (regulatory interpretation, risk assessment)

- Supply Chain (labelling, packaging, customs documentation)

4. Choose Partners Strategically

Select service providers who understand the interconnection between cross-border payments compliance and product compliance UK EU:

- Payment processors with multi-jurisdiction tax expertise

- Compliance consultancies with market entry experience

- Logistics providers familiar with customs requirements

- Accounting firms with cross-border VAT capabilities

5. Monitor Key Risk Indicators

Track metrics that signal potential compliance or payment issues:

- Customs clearance times (sudden increases indicate documentation problems)

- Payment dispute rates (high rates may indicate customer delivery issues)

- VAT reconciliation discrepancies (errors in tax calculation or reporting)

- Product return rates by market (may indicate compliance-related customer confusion)

6. Plan for Regulatory Changes

Both compliance and tax regulations evolve continuously. Build in:

- Quarterly regulatory review processes

- Budget reserves for unexpected compliance updates (5–10% of compliance costs)

- Relationships with local legal advisors

- Subscription to regulatory update services

Common Pitfalls to Avoid

Pitfall 1: Sequential Rather Than Parallel Planning

- The mistake: “We’ll get our payment infrastructure set up, then worry about compliance.”

- The consequence: Discovering product compliance UK EU requirements that necessitate repricing, relabelling, or reformulation after payment infrastructure is configured, requiring costly rework.

- The solution: Run compliance and cross-border payments compliance planning in parallel from day one, with regular integration checkpoints.

Pitfall 2: Underestimating Compliance Timelines

- The mistake: Assuming compliance can be achieved in 2–4 weeks.

- The consequence: Inventory arrives before compliance is complete, incurring storage costs and missed sales windows (particularly critical for seasonal products).

- The solution: Add 25% buffer to all estimated compliance timelines and plan inventory arrival accordingly.

Pitfall 3: DIY Compliance for Complex Products

- The mistake: Attempting to navigate complex regulatory frameworks — including responsible person ecommerce obligations — without specialised expertise.

- The consequence: Incomplete or incorrect compliance documentation leading to rejected shipments, marketplace suspensions, or sale of non-compliant products with liability exposure.

- The solution: Engage specialised compliance consultancies for category-specific expertise, particularly for regulated categories like cosmetics, supplements, electronics, and chemicals.

Pitfall 4: Ignoring Marketplace-Specific Requirements

- The mistake: Focusing solely on legal compliance while overlooking marketplace platform requirements.

- The consequence: Compliant products that cannot be listed on Amazon, eBay, or other platforms due to missing platform-specific documentation.

- The solution: Review marketplace seller requirements for your product category before finalising compliance strategy. Many platforms have requirements beyond legal minimums.

Pitfall 5: Single-Country Optimisation

- The mistake: Optimising payment and compliance strategy for one primary market (e.g., Germany) without considering implications for broader EU expansion.

- The consequence: Needing to repeat significant portions of setup work when expanding to additional countries, multiplying costs and delays.

- The solution: Build a scalable VAT compliance cross-border ecommerce and product compliance framework from the start, even if launching in a single market initially. Use OSS for VAT, work with pan-European RPs, and select payment providers with broad coverage.

Partnering for Success

Navigating the complexities of cross-border payments compliance and product compliance UK EU requires specialised expertise. The most successful market entries leverage partnerships that bring:

- Payment Expertise: Deep understanding of multi-jurisdiction tax requirements, local payment preferences, and currency management strategies. ExpandNow specialises in helping ecommerce brands optimise cross-border payment operations, ensuring seamless transactions and VAT compliance cross-border ecommerce at every stage.

- Compliance Expertise: Comprehensive knowledge of product-specific regulations across UK and EU markets, with established responsible person ecommerce infrastructure and database registration capabilities. Companies like Complizon, ExpandNow partner, provides full-service regulatory consultancy, managing every step from documentation to market entry for brands expanding into UK and EU markets.

- Integrated Approach: Partners who understand how compliance and payment challenges intersect, enabling coordinated solutions rather than siloed approaches.

The Bottom Line

Cross-border expansion into UK and EU markets offers tremendous growth potential for ecommerce brands, but success requires meticulous attention to both payment infrastructure and product compliance UK EU standards. These aren’t separate challenges, they’re two sides of the same market entry coin.

For finance directors, operations managers, and compliance officers, the key insight is this: cross-border payments compliance without product compliance is worthless, and product compliance without payment infrastructure is incomplete. Your market entry strategy must address both simultaneously, with clear ownership, realistic timelines, and adequate budgets.

Ensuring VAT compliance cross-border ecommerce obligations are met, appointing the right responsible person ecommerce representative, and integrating these with robust payment infrastructure is what separates brands that scale internationally from those that stall at the border.

The brands that thrive in cross-border ecommerce aren’t necessarily those with the best products or the biggest marketing budgets. They’re the brands that treat market entry as an integrated operational challenge, where compliant products flow seamlessly through borders and payment systems capture value efficiently across currencies and jurisdictions.

By following the frameworks, timelines, and best practices outlined in this guide, you can build a market entry strategy that mitigates risk, accelerates time to market, and sets the foundation for sustainable international growth.

How ExpandNow Can Help

ExpandNow makes cross-border selling simpler, safer, and more profitable.

As a Merchant of Record, ExpandNow takes on the legal and financial responsibility of selling internationally on your behalf — covering VAT compliance, local tax registrations, fraud prevention, payments, and daily payouts across the UK, EU, and beyond.

Brands that work with ExpandNow eliminate counterparty risk on their revenue, go live in new markets in weeks, and get full visibility into the unit economics of every market and channel. No hidden fees. No locked-in tech stacks. No compliance surprises.

Whether you’re launching internationally for the first time or replacing a legacy MoR provider, ExpandNow is built to grow with you.

Expanding internationally involves more than payments and compliance: market strategy, platform selection, and choosing the right Merchant of Record all play a critical role. For a practical deep-dive, read: How to Expand Ecommerce Internationally: 6 Insights from our Webinar